Fortune News | Feb 11,2023

May 3 , 2025.

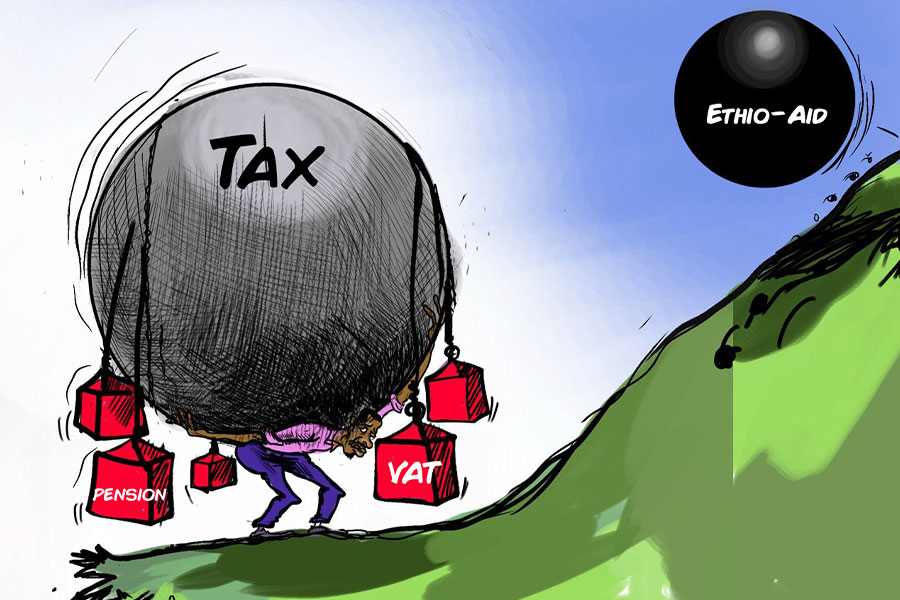

Pensioners have learned, rather painfully, the gulf between a figure on a passbook and a loaf of bread. A monthly allowance of 5,000Br (about 38 dollars at last week’s weighted average rate) used to keep senior retirees in groceries, rent, and a little dignity. Now it covers barely a day’s shopping. A recent study put it with cruel accuracy that, “pensioners are paying the government to hold their savings.”

Inflation still runs amok with close to 20pc year-on-year (YoY), while Treasury bill (T-bills) rates are stuck near 15pc; anyone forced into those bills loses money on every Birr. Forced is the word. Employees have poured roughly half a trillion Birr into the public and private schemes, which, together, sit on more than 450 billion Br. Rules cover about 60pc, often more, into low-yield government paper. Each percentage point of lost yield on that hoard costs future pensioners 4.5 billion Br a year.

Employers put up 11pc of pay, employees seven percent and the armed forces a chunky 25pc. On paper, an employee who stays 30 years can retire on 70pc of their final salary, but rising prices make the promise slippery. Laws passed in 2022 lowered the indexation interval and, in theory, opened the investment menu. In practice implementation has stalled.

Coverage is wafer-thin. The schemes capture barely eight percent of the labour force and only 14pc of the elderly. A voluntary micro pension with flexible payments could widen the base. Experience elsewhere shows informal workers would save if fees are low and accounts portable. A bigger contributor pool would ease the future dependency ratio and steady the books.

For all the spreadsheets, pensions are about people. Middle managers who have paid diligently for decades deserve more than a stipend that melts at the market stall. Young factory hands should believe that today’s deductions will become tomorrow’s safety net. Ethiopia enjoys a demographic sweet spot. Contributors now outnumber pensioners, and assets are swelling. Waste that window, and the country will face the ugly choice of cutting benefits or raising taxes.

The mismatch between need and performance is already creeping. Close to 750,000 public sector retirees and a fast-growing band in the private sector see contributions dwarf payouts. In 2023, the Public Servants’ Social Security Administration collected 30.5 billion Br but paid out only 8.4 billion Br, pushing reserves past 300 billion Br. Profits were slightly over one billion Birr, a real return of barely four percent.

Why so timid?

Blame a legal straightjacket. Decrees dating from Emperor Haile Selassie’s reign lock pension cash into “safe” government paper. Even proclamations 1267 and 1268 of 2022 opened the door only a crack. Boards still packed with government appointees choose caution. The Ethiopian Securities Exchange (ESX), inaugurated in January this year and desperate for anchor investors, finds the pension giants holding less than five percent of their assets outside public debt or overnight bank deposits.

Peer markets show what is possible. Nigeria’s reformed scheme, launched in 2004, has swollen to roughly 14.6 billion dollars with almost 40pc of assets outside federal bonds. Its capital props up Lagos’s markets, and PenCom, a strict watchdog, caps fees and sets age-based bands. Returns only edge past inflation, yet Nigerian savers still beat Ethiopians by three to four percentage points yearly.

The Ethiopian row is ideological, not arithmetic. Union leaders, senior bureaucrats and social policy scholars voice three fears: markets can crash, private managers may gouge savers, and the state will forfeit a cheap loan. The Private Organisations Employees' Social Security Administration is chaired by Teklewold Atnafu, a former central bank governor, now senior monetary policy advisor to the Prime Minister, with Kassahun Folo of the trade union confederation and Fiteh Woldesenbet (PhD) of the employers’ federation on its board. They should admit that compound interest is beating them.

A collapse would hit a treasury already juggling a debt-to-GDP ratio above 50pc and a tricky Eurobond renegotiation. Shielding pensioners from market swings may feel safe; shielding them from mathematics is impossible.

A prudent cure is staged liberalisation.

Licensed, well-capitalised managers such as domestic banks, insurers and foreign joint ventures could bid for slices of the existing portfolios, against tight fee caps and benchmarks set by the National Bank of Ethiopia (NBE). Savers would choose among three default lifecycle funds instead of being locked in one vast pot. Younger workers would sit in growth portfolios heavy on equities and infrastructure; near retirees would shift to safer bonds.

However, supervision should be stiffened before the first Birr moves. The Ethiopian Capital Market Authority (ECMA), led by Hana Tehelku, should gain explicit pension oversight and hire actuaries and forensic accountants at market rates. A quarterly performance dashboard, strict accounting standards, and rapid sanctions would build trust. Transparency, not bureaucracy, is the antidote to mistrust.

Transition costs can be managed. Workers within a decade of retirement could stay in the old formula, sustained by a closing pool. Younger staff would shift to funded accounts, with 20-year recognition bonds covering past service. A small floor pension worth 15pc of median wages would guard against destitution.

The payoff is hefty. If half of today’s 450 billion Br hoard moved into a diversified portfolio targeting a real return of four percent, conservative by global norms, the extra yield over present negative return bills would exceed 25 billion Br a year. Compounded for 15 years, the difference grows past 600 billion Br, enough to fund every pensioner at the current minimum for a decade.

Early experiments already pay off. A modest purchase of bank shares and development bank bonds earned 7.2 billion Br in one year, 130pc above target and triple the five-year average. Tilahun E.Kassahun (PhD), head of the ESX, foresees a 100 billion Br market value within five years; a 15pc pension allocation could more than double that.

Fee gouging could be a real risk, but easy to curb. An all-in-charge capped at one percent — Nigeria’s average is 0.88pc and falling — would keep managers honest. Minimum cash buffers and countercyclical allocation floors would tame liquidity shocks. Micro pension enrolment could ride on national ID cards (Fayida) and mobile money wallets. Talent, scarce today, follows money.

Such reform could fit Prime Minister Abiy Ahmed (PhD) Administration's broader liberal agenda. Telecoms, logistics, and banking are opening. A credible pension road map would deepen capital markets, free space on the budget, and please the IMF, which wants more domestic buyers for public debt. It could unlock concessional cash and soothe rating agencies fretting over hidden liabilities.

Still, politics remain delicate. Unions bruised by wage freezes will not swallow uncertainty. The tonic is sunlight, putting labour representatives and re atirees’ groups on the supervisory board, promising that no benefits already in payment can fall, and publishing dashboards each quarter. Resistance could linger, but negative real yields and a looming demographic bulge make stubborn allies for reformers.

History counsels urgency. In 1961, civil servants paid four percent and the state six percent. The military regime kept the scheme but cut retirement to 55. A 1975 decree swept nationalised firms into the pool. A 2003 statute lifted rates, and laws(714 and 715) passed in 2011 drew in private workers. The 2022 proclamations pledged diversification, yet progress has dragged.

It is wise to recognise that Ethiopia has a fleeting chance. The funds are asset-rich and liability-light, buoyed by a young workforce. Leave the hoard in bills, and it will wither; invest it through disciplined competition, and it can finance infrastructure, reward savers, and deepen markets. The choice is between managed risk and inevitable decline. The clock is ticking, and every lost month robs savers of the compound growth they desperately need later.

PUBLISHED ON

May 03,2025 [ VOL

26 , NO

1305]

Fortune News | Feb 11,2023

Radar | Oct 15,2022

Radar | Sep 28,2019

Commentaries | Dec 25,2018

Featured | Nov 23,2019

My Opinion | 130157 Views | Aug 14,2021

My Opinion | 126456 Views | Aug 21,2021

My Opinion | 124459 Views | Sep 10,2021

My Opinion | 122213 Views | Aug 07,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

May 31 , 2025 . By BEZAWIT HULUAGER

Real-estate developers have formed a new lobbying group, the Ethiopian Real Estate De...

May 31 , 2025 . By NAHOM AYELE

A draft proclamation, endorsed by the Council of Ministers two weeks ago, will permit...

May 31 , 2025 . By BEZAWIT HULUAGER

Regulators at the National Bank of Ethiopia (NBE) have issued a notice to commercial...

May 31 , 2025 . By NAHOM AYELE

The Ministry of Water & Energy has announced plans to enlist institutions located...

Loading your updates...

Loading your updates...