Over the last two weeks we have seen just how uncommon the CAP has become across Europe. The flexibility brought in to ensure the CAP reform went through has allowed countries to target their aid more than ever at different regions and different sectors.

Countries can also use their Pillar II funds under rural development to push money into different areas. Ireland is doing it with Areas of Natural Constraints, but also with schemes such as the Beef Data and Genomics Programme, which 29,000 farmers have joined.

We have also seen the dismantling of the safety nets that were once there for beef and milk in particular. Elements of income protection were brought in under the new CAP but there has been little uptake on the measures. After the latest bout of price volatility, there will be more focus on this area. The European Commission has clearly shown that there is no desire to bring back intervention in any large way, but other avenues will be explored. We are also seeing a move towards protection around food security in other major countries.

It is important to remember CAP is only one element of EU intervention, albeit the most important. Nitrates regulations continue to have a big impact in countries such as the Netherlands and Denmark, and this will not change. National policies such as those on renewable energy in some countries have seen farmers make decisions not solely based on the profitability of their current system. You just have to look at Germany and more recently the UK to see how the slurry can be more profitable than the cows when an anaerobic digestor is installed on a farm.

One thing we know from the past is that the impact of CAP reform will not be immediately apparent. There will be a time delay as farmers react to the different policies and farming practices change across Europe.

When decoupling first came in, it was predicted that the suckler herd would collapse. That didn’t happen.

The biggest factor for us will be on how our neighbours and biggest trading partner, the UK, reacts.

The increase in coupling to 10% will have the biggest effect. If small French farmers are getting a higher direct payment and up to €200 per suckler cow, they will not be as affected by swings in market prices.

In Europe, everything is intertwined – and CAP is no different. Each farmer will have to look at their own system and where their products end up to see how CAP affects them.

But what countries get the CAP money?

The overall CAP budget is €55.7bn a year. Despite being cut for the first time, the percentage spent on CAP has actually increased to 41% of the overall EU budget, which suffered higher overall cuts.

Big four still get nearly 50% of CAP

To see what countries get the funds and how their farmers are benefiting, I have broken it down not just by country but also by hectare and most importantly what each farmer is getting in the different countries across Europe.

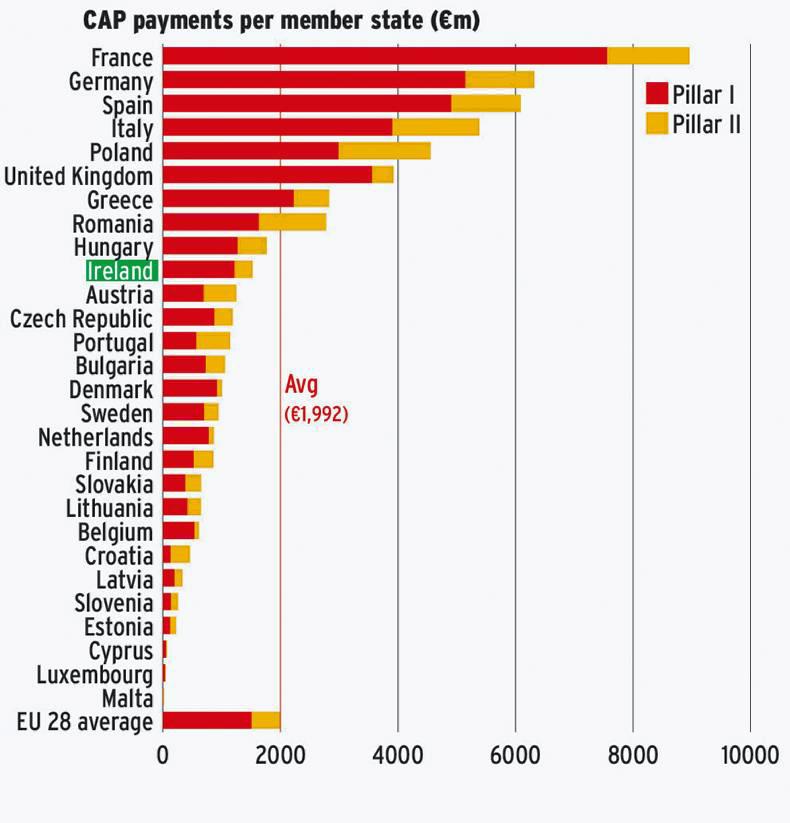

By country

France at nearly €9bn still gets the biggest slice of the CAP pie. Germany, Spain and Italy are next, with the top four accounting for 48% of the overall budget.

They are surprisingly followed by Poland – its large fund for Pillar II pushed it above the UK. You can see why Poland moved to transfer 25% of Pillar II funds into Pillar I, while some UK countries are moving funds from Pillar I to bolster the small Pillar II pot. The one issue the graphic does not show is what national funding each country is using to bolster its Pillar II pot. Ireland with 46% co-funding will be at the top end of the list but some countries could put in less than 20% co-funding.

For farmers in each country it is not the size of the overall pot that is most important. The eligible hectares and the funds per farmer are much more relevant. For this we look to the number of eligible hectares in each country and also the number of farmers.

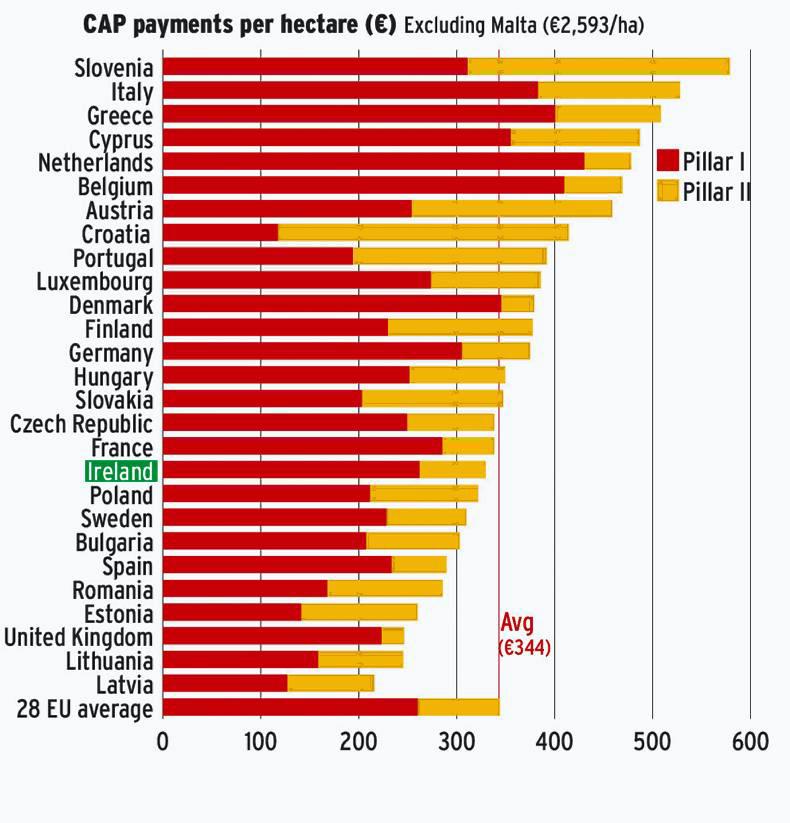

Per hectare

The payment per hectare and per farmer is still very different.

While redistribution between and within countries will reduce this, there will still be major differences by 2020.

These graphs show very different pictures. On a per-hectare basis (excluding Malta), the Netherlands has the higher Pillar I payment of €430/ha while Croatia has the lowest at €117/ha. Croatia has the highest Pillar II payment of €297/ha (also excluding Malta), with the lowest in the UK at just €23/ha. Combining both pillars gives Slovenia the higher overall payment per hectare, followed by Italy and Greece. The lowest are in Latvia, Lithuania and the UK. It shows that it is not just an east versus west issue in the current CAP reforms.

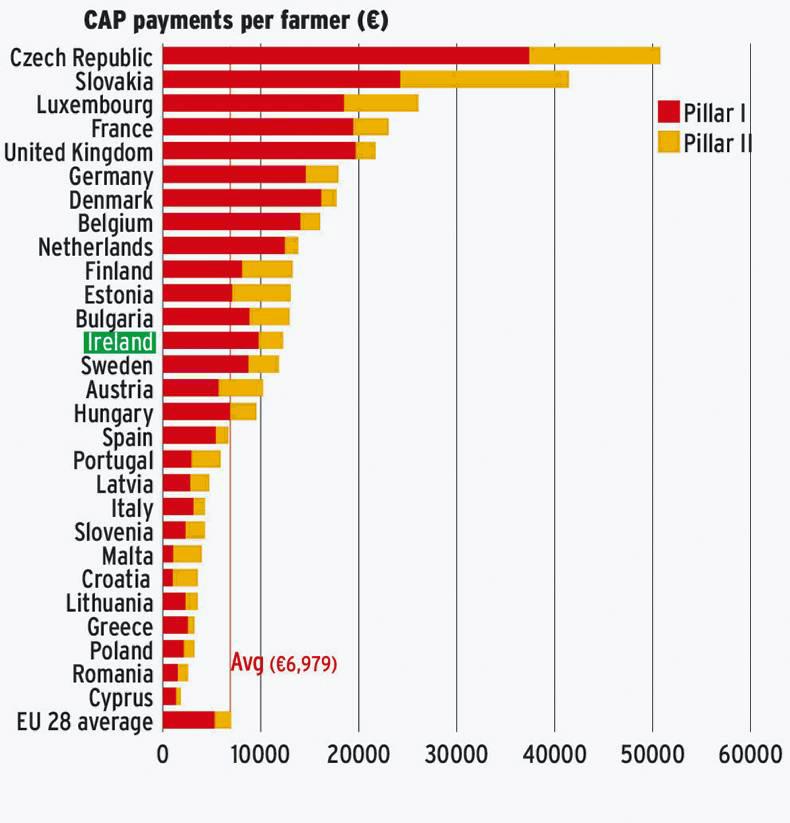

Per farmer

Payment per farmer is even more interesting. Looking across Europe there are around 800,000 farmers farming an average 20ha each. They get €5,276 under Pillar I and €1,703 under Pillar II a total close to €7,000 from the EU each year.

Farmers in the Czech Republic stand out. While the country has a lower Pillar I payment per ha (€249) than Ireland (€260), the large average holding of 80ha means the farmers in the country get by far the largest payments of €37,000 under Pillar I and €50,000 in total. Slovakia is next due to very high Pillar II payments, with farmers in Luxemburg benefiting due to scale. Irish farmers at €12,200 are well above the EU average. Interestingly, Poland, which gets the fifth biggest pot of money, is well below it (€3,239). This is because there are 1.4m Polish farmers with an average farm size of just 6ha. There is a move there to target farmers over 3ha to ensure the money has greater impact for full-time farmers

Read more

Uncommon CAP series: Uncommon CAP series: the impact of national CAP implementation choices across the EU

Over the last two weeks we have seen just how uncommon the CAP has become across Europe. The flexibility brought in to ensure the CAP reform went through has allowed countries to target their aid more than ever at different regions and different sectors.

Countries can also use their Pillar II funds under rural development to push money into different areas. Ireland is doing it with Areas of Natural Constraints, but also with schemes such as the Beef Data and Genomics Programme, which 29,000 farmers have joined.

We have also seen the dismantling of the safety nets that were once there for beef and milk in particular. Elements of income protection were brought in under the new CAP but there has been little uptake on the measures. After the latest bout of price volatility, there will be more focus on this area. The European Commission has clearly shown that there is no desire to bring back intervention in any large way, but other avenues will be explored. We are also seeing a move towards protection around food security in other major countries.

It is important to remember CAP is only one element of EU intervention, albeit the most important. Nitrates regulations continue to have a big impact in countries such as the Netherlands and Denmark, and this will not change. National policies such as those on renewable energy in some countries have seen farmers make decisions not solely based on the profitability of their current system. You just have to look at Germany and more recently the UK to see how the slurry can be more profitable than the cows when an anaerobic digestor is installed on a farm.

One thing we know from the past is that the impact of CAP reform will not be immediately apparent. There will be a time delay as farmers react to the different policies and farming practices change across Europe.

When decoupling first came in, it was predicted that the suckler herd would collapse. That didn’t happen.

The biggest factor for us will be on how our neighbours and biggest trading partner, the UK, reacts.

The increase in coupling to 10% will have the biggest effect. If small French farmers are getting a higher direct payment and up to €200 per suckler cow, they will not be as affected by swings in market prices.

In Europe, everything is intertwined – and CAP is no different. Each farmer will have to look at their own system and where their products end up to see how CAP affects them.

But what countries get the CAP money?

The overall CAP budget is €55.7bn a year. Despite being cut for the first time, the percentage spent on CAP has actually increased to 41% of the overall EU budget, which suffered higher overall cuts.

Big four still get nearly 50% of CAP

To see what countries get the funds and how their farmers are benefiting, I have broken it down not just by country but also by hectare and most importantly what each farmer is getting in the different countries across Europe.

By country

France at nearly €9bn still gets the biggest slice of the CAP pie. Germany, Spain and Italy are next, with the top four accounting for 48% of the overall budget.

They are surprisingly followed by Poland – its large fund for Pillar II pushed it above the UK. You can see why Poland moved to transfer 25% of Pillar II funds into Pillar I, while some UK countries are moving funds from Pillar I to bolster the small Pillar II pot. The one issue the graphic does not show is what national funding each country is using to bolster its Pillar II pot. Ireland with 46% co-funding will be at the top end of the list but some countries could put in less than 20% co-funding.

For farmers in each country it is not the size of the overall pot that is most important. The eligible hectares and the funds per farmer are much more relevant. For this we look to the number of eligible hectares in each country and also the number of farmers.

Per hectare

The payment per hectare and per farmer is still very different.

While redistribution between and within countries will reduce this, there will still be major differences by 2020.

These graphs show very different pictures. On a per-hectare basis (excluding Malta), the Netherlands has the higher Pillar I payment of €430/ha while Croatia has the lowest at €117/ha. Croatia has the highest Pillar II payment of €297/ha (also excluding Malta), with the lowest in the UK at just €23/ha. Combining both pillars gives Slovenia the higher overall payment per hectare, followed by Italy and Greece. The lowest are in Latvia, Lithuania and the UK. It shows that it is not just an east versus west issue in the current CAP reforms.

Per farmer

Payment per farmer is even more interesting. Looking across Europe there are around 800,000 farmers farming an average 20ha each. They get €5,276 under Pillar I and €1,703 under Pillar II a total close to €7,000 from the EU each year.

Farmers in the Czech Republic stand out. While the country has a lower Pillar I payment per ha (€249) than Ireland (€260), the large average holding of 80ha means the farmers in the country get by far the largest payments of €37,000 under Pillar I and €50,000 in total. Slovakia is next due to very high Pillar II payments, with farmers in Luxemburg benefiting due to scale. Irish farmers at €12,200 are well above the EU average. Interestingly, Poland, which gets the fifth biggest pot of money, is well below it (€3,239). This is because there are 1.4m Polish farmers with an average farm size of just 6ha. There is a move there to target farmers over 3ha to ensure the money has greater impact for full-time farmers

Read more

Uncommon CAP series: Uncommon CAP series: the impact of national CAP implementation choices across the EU

This is a subscriber-only article

This is a subscriber-only article

SHARING OPTIONS: