Call it a work in progress.

As the global financial system continues a long, slow healing process, the echoes of the implosion inflicted by the credit collapse of 2008 are fading into history.

Yet five years after the worst financial crisis since the Great Depression, a pitched political and regulatory battle is still being fought over multiple provisions of a far-reaching series of reforms and regulations, known as Dodd-Frank, that were designed to prevent a recurrence. (Tweet This)

"The financial crisis crushed the American economy and devastated American taxpayers, households and businesses and that's what we cannot afford to have," said Michael Barr, a University of Michigan law professor and former Treasury official who as a key architect of the law. "Dodd-Frank and other reforms are making the system safer and fairer and that's exactly what we need."

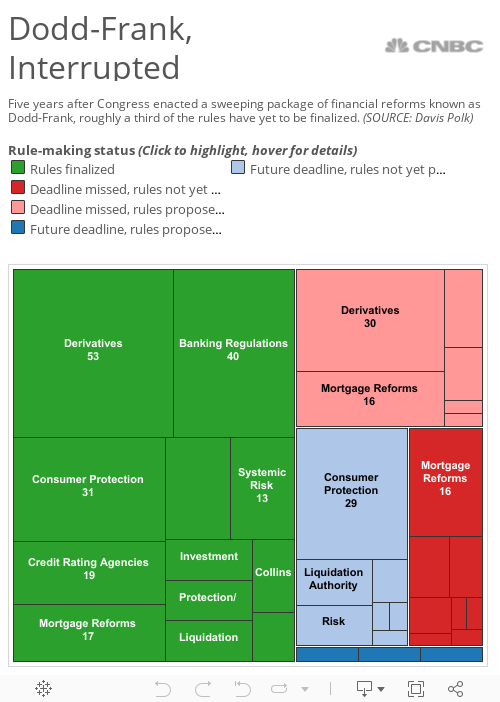

But five years after Dodd-Frank was enacted, roughly 40 percent of the nearly 400 proposed rules required under the 850-page law have yet to be finalized. A fifth of them haven't even been proposed, according to Davis Polk & Wardwell, a law firm that has tracked the Dodd-Frank rule-making progress since the law was enacted.

And with many of the bill's original supporters in Congress no longer in office and the urgency of the 2008 financial crisis fading from public memory, the law has recently come under attack from multiple fronts as well-heeled corners of the financial services industry seek to have rules delayed, watered down or revoked.

"For most of the short life of Dodd-Frank, there has been an aggressive campaign to repeal it," Treasury Secretary Jack Lew said at a Brookings Institution appearance earlier this month. "We're seeing proposed changes that are in the name of simplifying it that would actually go at the heart of some of the protections that we've put in place."

From the beginning, the debate over how to create new regulations to prevent another financial meltdown was one of the most contentious of the past decade, pitting reform-minded Democrats against free market Republicans aided by an army of lobbyists on all sides.

The resulting Dodd-Frank Wall Street Reform and Consumer Protection Act—named for former Democratic Rep. Barney Frank and former Democratic Sen. Christopher Dodd—was a sprawling, kitchen sink of proposed regulations, signed by President Barack Obama in July 2010, which contained 17 separate sections, governing everything from car loans to CEO pay to Congolese conflict minerals.

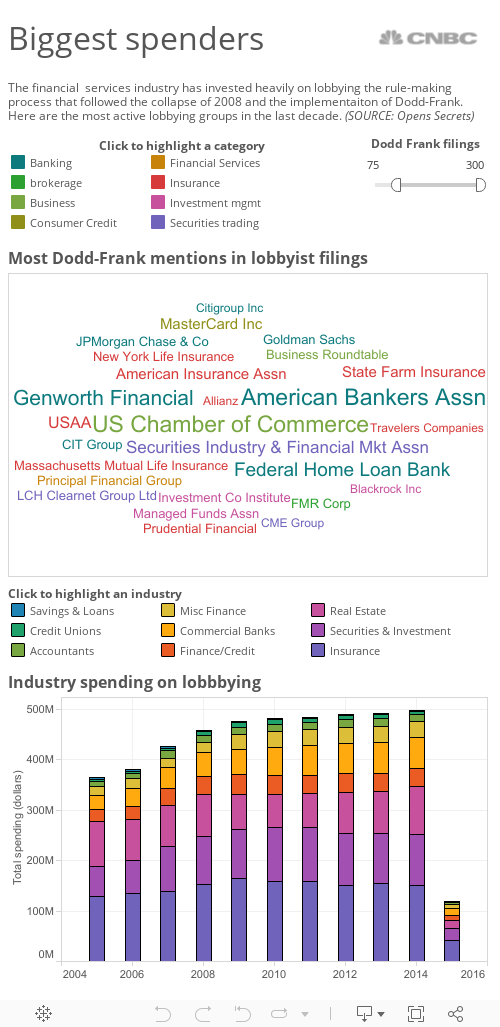

The creation of the legislation governing the well-funded financial services industry fueled a massive lobbying effort that continues as the rule-making process drags on.

While sweeping in scope, the law Congress enacted left the details of specific rule-making to a patchwork of regulatory agencies, including a newly created Financial Stability Oversight Council designed to coordinate the rule-making process. A new Consumer Financial Protection Bureau, an independent consumer lending watchdog, consolidated regulatory powers once housed in seven different federal agencies with a mandate to protect individuals from abusive lending practices by the financial services industry.

With hundreds of new rules being written by multiple agencies, the law became a ripe target for a group of well-paid lobbyists. That's one reason that, despite specific deadlines attached to many of the new rules, Dodd-Frank remains a work in progress.