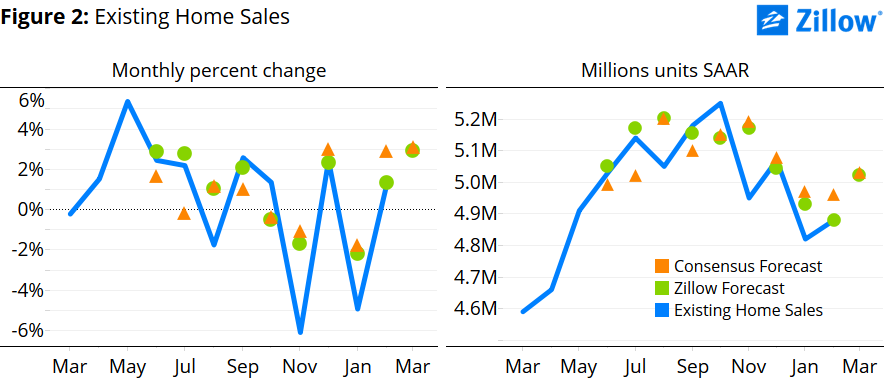

- Zillow expects existing home sales to rise 2.9 percent to 5.02 million units (SAAR) in March.

- Expectations of rising interest rates and home prices within the year may be hastening the buying decision of home shoppers and, along with a strengthening labor market and rising demand from millennials, could lead to rising sales in the next few months.

Zillow expects Wednesday’s March existing home sales data from the National Association of Realtors (NAR) to show an increase of about 2.9 percent, to a seasonally adjusted annual rate (SAAR) of 5.02 million units, up from 4.88 million units (SAAR) in February.

Background

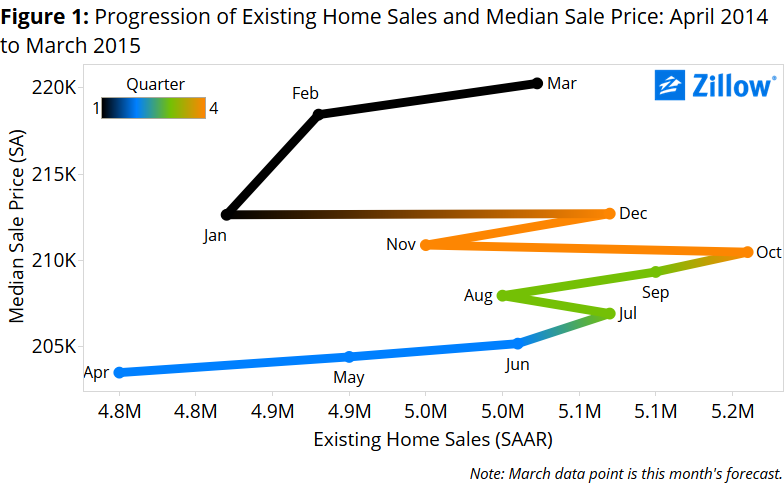

There are signs that existing home sales could be looking up at the end of the first quarter, despite a slow start. After sales stalled somewhat in the second half of 2014 – even as prices continued to rise – sales and prices both rose in February from January, up 1.3 percent and 2.7 percent, respectively (figure 1)[i]. Real median household income also started to rise in 2013 and 2014 after continual declines since 2008, thanks to a tightening labor market just 0.2 percentage points away from full employment[ii].

Interest rates are again making headlines. Although mortgage rates remain near historic lows, the Federal Reserve Board is expected to lift the floor for short-term interest rates as early as this summer or early fall. Lenders and homebuyers could be considering this now as they set interest rates and make buying decisions, even though there has not yet been any change in Federal Reserve policy. Expectations for future rate hikes may be one reason why the rate on a 30-year fixed-rate mortgage remained steady at 3.71 percent in January and February, but increased 6 basis points in March, after steadily falling throughout 2014.[iii]

Higher mortgage interest rates, along with rising home prices, an improving labor market, growing incomes and increasing demand from millennials, may also be contributing to the recent rise in pending home sales. Pending sales fell 1.5 percent in December, but rebounded 4.3 percent in February compared to December. As a result, we could see home sales continue to rise over the next few months as those actively seeking to buy a home move their timeline forward to take advantage of both the (even perceived) “last days” of historically low rates and before prices rise further, in hopes of keeping financing costs low.

March Forecast

Our existing home sales forecast uses a best-fit combination of two models, a structural model and a historical model. The models are in agreement this month, with both pointing towards higher sales.

The structural model suggests very little change in existing home sales, up just 0.6 percent month-over-month to 4.91 million units (SAAR). According to this model, rising mortgage interest rates and prices, combined with movements in underlying fundamentals at the end of 2014 that are again expected to cancel each other out, should result in home sales having very little change from February.

The historical model suggests an increase of 3.2 percent, to 5.04 million units (SAAR). Pending home sales rose in January and February, reaching the highest level since June 2013. Pending home sales have been on the rise since early 2014, and these recent movements combined with similar movements in existing home sales result in a strong positive forecast for March.

Using a best-fit combination of the two models, we obtain a point forecast of 5.02 million units (SAAR), a rise of 2.9 percent from February (figure 2).

[i] We forecasted March’s median sale price using a best-fit ARIMA model – an ARIMA (5,1,0) in this case – to get a sense of the where the housing market will be this month in terms of a supply and demand framework. This forecast produced a median sale price to $220,300 and is represented along with our sales forecast for March in figure 1.

[ii] Full employment is defined as actual unemployment equal to the natural rate of unemployment. The actual unemployment rate for 2015 Q1 is 5.6 percent and the natural rate of unemployment is estimated to be 5.4 percent. Unemployment needs to drop just 0.2 percentage points to reach full employment. Data used comes from the Federal Reserve Economic Data of the St. Louis Federal Reserve Bank.

[iii] According to Primary Mortgage Market Survey data provided by Freddie Mac.