Uncategorized

Mortgage Rates in 2016: Gradually, Then Suddenly

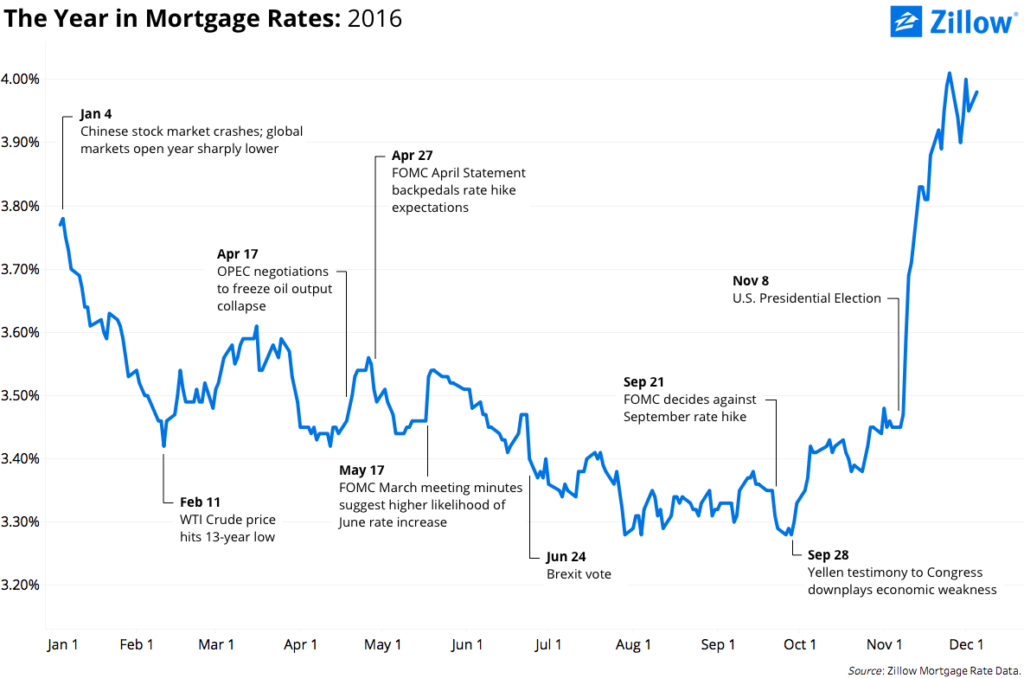

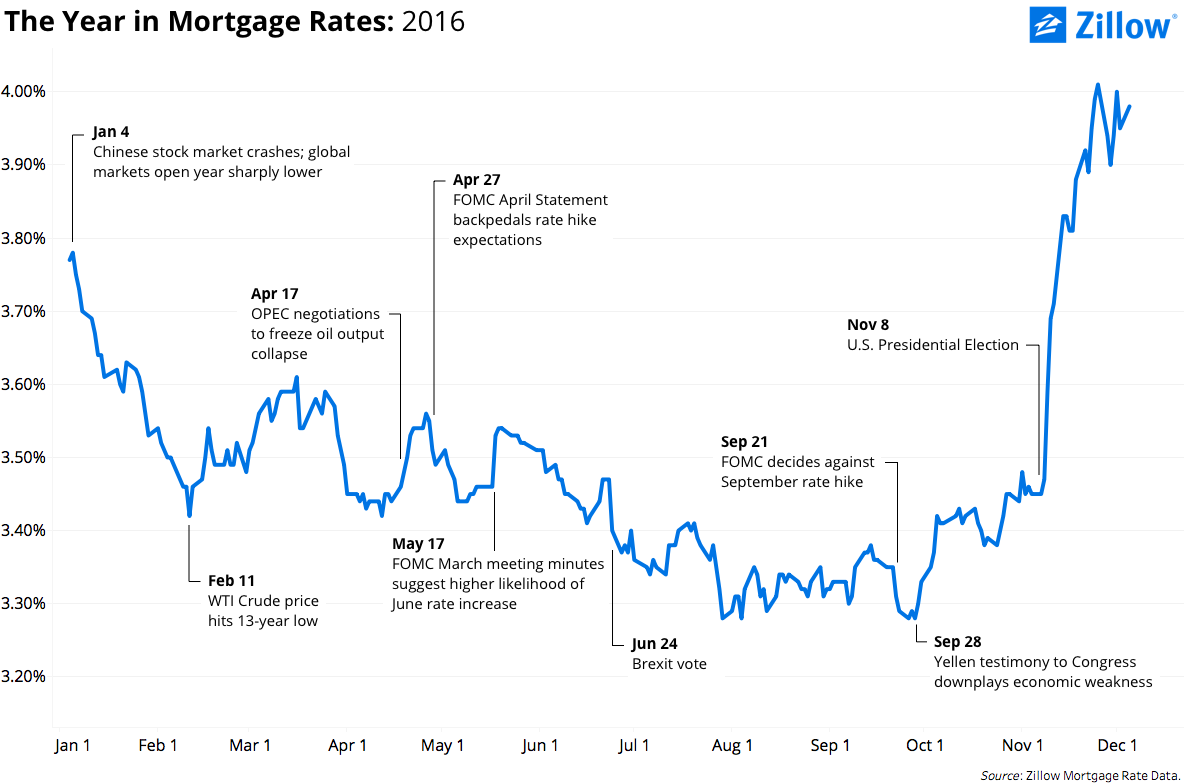

At the start of 2016, expectations were high for mortgage rates. Following the Federal Reserve Board’s December 2015 rate hike, the first in a decade, financial markets expected mortgage rates to steadily inch higher with a series of three to four more Fed rate hikes over the year. Instead, mortgage rates followed the famous path to bankruptcy described by Ernest Hemingway: They moved gradually, then suddenly.

At the start of 2016, expectations were high for mortgage rates. Following the Federal Reserve Board’s December 2015 rate hike, the first in a decade, financial markets expected mortgage rates to steadily inch higher with a series of three to four more Fed rate hikes over the year. Instead, mortgage rates followed the famous path to bankruptcy described by Ernest Hemingway: They moved gradually, then suddenly.

Buffeted by a seemingly endless series of geopolitical shocks that pushed global investors toward safe assets and, as a consequence, pushed U.S. mortgage rates toward historic lows, mortgage rates moved gradually lower for much of the year before very rapidly turning course.

In January, markets opened with a bang as Chinese stock markets crashed on the first trading day of the year, which spilled over into global financial markets. Mortgage rates fell by about 20 basis points during the ensuing two weeks. When China reported its Q4 2015 GDP growth data in mid-January – its lowest since 1990, in a country where economic growth has historically been (rightly or wrongly) associated with political stability – the slide continued. Mortgage rates fell another 20 basis points by mid-February.

With financial markets in turmoil, global oil prices also dove, continuing a two-year slide in the face of unexpectedly weak demand and technology-fueled new supply. The spot price for West Texas Intermediate crude hit a 13-year low on February 11th, the same day mortgage rates also hit a temporary low.

By springtime, geopolitics took a (temporary) backseat to monetary policy. Fed officials have repeatedly emphasized that monetary policy normalization – that is, the gradual rise in interest rates toward levels associated with a more “normal” economy – would be “data dependent,” contingent on incoming economic data. But data dependence can be a deceptively simple mantra if taken as is: Some degree of data interpretation is almost always necessary. By March, financial markets were grappling with exactly how the Fed would interpret the most recent economic data.

This confusion was not aided by Fed officials’ very public (for the Fed, anyway) deliberations. In a March 29 speech to the Economic Club of New York, Fed Chair Janet Yellen spoke about “global risks” to the U.S. economic outlook, and mortgage rates subsequently fell by about 15 basis points. Rates climbed back in mid-April after several speeches by other FOMC voters downplayed global risks, only to give those gains back again after the FOMC’s April statement backpedaled rate hike expectations. Two weeks later, when the April meeting minutes were made public, markets seemed to sense a discrepancy between public comments and the written record. Rates jumped again. The same data-driven indecision would play out again in the fall over the committee’s September decision not to raise interest rates.

Geopolitical events again grabbed the headlines in June as the United Kingdom unexpectedly voted to exit the European Union, fueling a fresh round of global capital flight to safe assets and pushing mortgage rates down by 15 to 20 basis points over the next six weeks as the dust settled.

Geopolitical events again grabbed the headlines in June as the United Kingdom unexpectedly voted to exit the European Union, fueling a fresh round of global capital flight to safe assets and pushing mortgage rates down by 15 to 20 basis points over the next six weeks as the dust settled.

Of course, the largest financial market shock of the year was the U.S. presidential election. The political uncertainty sparked by the election of Republican Donald Trump – contrary to most polls and market predictions – prompted mortgage rates to spike toward two-year highs. In the three days after the election, mortgage rates jumped by roughly the same magnitude as they had fallen between early January and mid-February in the face of global stock market turmoil, and then proceeded to jump further. In the eleven trading days from November 7 to November 23 – the day before the election through the day before Thanksgiving – the average 30-year, fixed mortgage rate for a borrower with good credit seeking a conforming loan with a down payment of 20 percent rose 50 basis points to 3.95 percent.

A year after the first Fed rate hike in a decade, markets are now expecting – again in December – just the second rate hike in a decade. Before November, markets’ high expectations for mortgage rates in 2016 seemed laughable in retrospect. But a late-year political surprise has made year-ago expectations somewhat more reasonable, if for unexpected reasons.

{kind=link}