Why do so many people think buying a house is part of the American Dream?

The cultural programming around buying a house—not renting—is so strong, most people don’t even realize where it comes from. Our parents tell us “real estate is the best investment.” Schools teach it. Even the government encourages us to buy.

I’d like to talk about the lies, cover-ups and half-truths about real estate. Housing can be a great investment, but usually it’s not. And almost nobody runs the real numbers when they buy.

Would it surprise you to know that if there are two equally expensive houses—one for rent, one to buy—the person who buys will pay 40 percent to 50 percent more each month? That’s what happens when you factor in property taxes, insurance, maintenance fees and assorted fees like repairs—which almost nobody does.

Buying a house is the largest purchase of your life. You shouldn’t believe phrases like “I’m throwing money away on rent” or “Why would I pay my landlord’s mortgage?”

The truth is, most of what we’ve been raised to believe about owning a house simply isn’t true.

A mortgage is much, much more expensive than rent

We all seem to ignore common sense when it comes to purchasing a house.

Consider the reader who once told me, “Oh, I pay $1,000 a month renting my apartment, so I can definitely afford $1,000 a month on a mortgage and build equity.”

I asked her, “How nice is your apartment?” She admitted that the hardwood floors are a bit old and kitchen is way outdated.

“So will you want a house like that, or will you want a nicer place? One with recessed ceilings, newer appliances, a balcony large enough for entertaining?”

She looked at me as if I were an idiot. “Of course I want a nicer house.”

“O.K. But that will probably cost more than your current rent, right?”

The lightbulb went off in her head.

Chances are you’ll want a nicer house than the apartment you’re currently renting. All of that means the monthly payment will be higher.

That’s pretty obvious. But it’s only the starting point.

A house is rarely a smart investment

“But Ramit,” you might say. “Buying a house is an investment! I’m tired of throwing my money away on rent.”

I’m convinced this awful phrase—“I don’t want to waste money paying rent”—was invented by realtors because it’s simply not true for many people.

That’s right: You are not wasting rent if you live in an expensive area. And since most of you reading this likely live in a major city with an expensive real estate market, let me repeat that: You are NOT wasting rent right now.

Americans’ biggest “investments” are their houses—and real estate is also the area where Americans lose the most money.

Realtors (and many homeowners) are going to flood my inbox with hate mail for saying this, but in truth, real estate is the most overrated investment in America. It’s a purchase first—a very expensive one—and an investment second.

And the returns on that investment are mediocre, at best.

Run the numbers. Yale economist Robert Shiller found that from 1890 to 1990, the return on residential real estate was just about zero after inflation.

ZERO.

What’s interesting is you get people who say things like, “I bought my house in 1970 for $45,000, and now it’s $445,000. I made $400,000 profit!”

Not true. They forget about phantom costs.

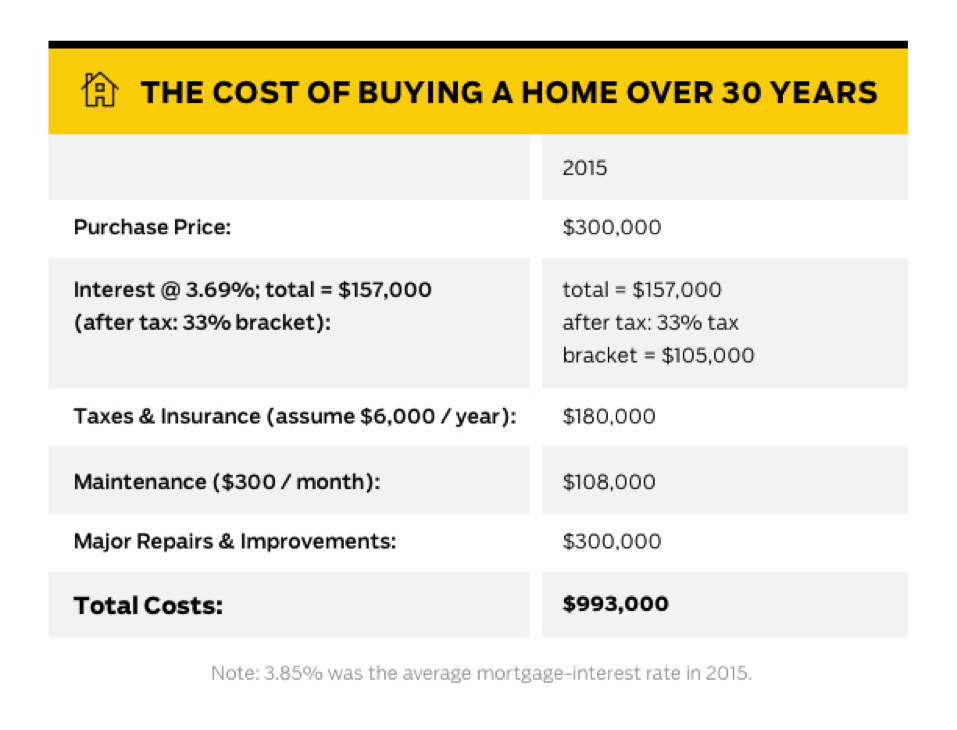

It costs way more than you think

When you buy a house, you won’t only pay the mortgage each month. You’ll also owe property taxes, insurance and maintenance fees that will add hundreds per month to your living expenses.

I call these “phantom costs.”

When you rent, if something breaks or the hot

(By the way, don’t ever let someone tell you, “You’re just paying your landlord’s mortgage. If they were losing money, they wouldn’t rent it!” Wrong: Your landlord can only charge what the market will bear. Many landlords are losing money every month. A surprisingly high number don’t even realizing it.)

When you own, you have to fix things or call someone to fix them for you. And of course you pay for it yourself.

That a plumber here and there doesn’t sound so bad. But imagine that in the course of owning a house, if your roof breaks, that’s $25,000. You have to amortise that out over the entire cost of the house.

Let’s dig into this some more.

Say you pay $1,000 per month renting. Even if your mortgage is the same $1,000 per month as your rent, when you own, you have to add 40 percent to 50 percent to that monthly amount to factor in all those phantom costs. Now you’re paying closer to $1,500 a month.

And if you buy a $300,000 house today, over 30 years, it could cost you almost $1 million.

Does spending $1 million seems like such a great investment now?

Being a homeowner impacts every part of your life

If phantom costs aren’t enough to scare you away, how about this: Buying a house—even the one in your ideal town, in the perfect school district, with every feature you’ve ever dreamed of—can keep you from living what I call a Rich Life. That’s a life where you get to travel, spend time with your family, hire someone to cook your meals and pretty much do whatever you want.

How does having the ideal house prevent your other dreams from happening?

No matter what, you have to make your monthly payment every single month—if not, you’ll lose your perfect house and watch your credit tank.

This affects the kind of job you take and your level of risk tolerance. And it means you’ll need to save for a six-month emergency plan in case you lose your job and can’t pay your mortgage.

And that could mean sitting behind a desk in a suit working like a robot rather than running your own online business from the beach as you watch your kids play in the ocean or taking two months off to backpack through Europe with your sister.

I’m known for saying you don’t need to give up your morning latte to save money. Why would I tell you to give up your dream job or investing in smarter things just to own a house?

Leverage and tax savings aren’t what they seem

Whenever I ask someone, “Why do you want to buy a house?” there are two other common replies that people don’t seem to fully understand. Like the American Dream, these myths cannot seem to die.

I’m talking about leverage and tax savings. And both could cause you to lose money.

1. Leverage works both ways

Homeowners will often point to leverage as the key benefit of real estate. In other words, you can put $20,000 down for a $100,000 house, and if the house climbs to $120,000, you’ve effectively doubled your money.

That sounds great, but it’s ignoring one big thing: The price of a house doesn’t always increase. So unfortunately, leverage can also work against you if the price goes down.

And while the math is obvious when the value of your house rises, there are hidden costs to consider if the value of your house falls.

If your house declines by 10 percent, you don’t just lose 10 percent of your equity—it’s more like 20 percent once you factor in the 6 percent realtor’s fees, the closing costs, new furniture and other expenses.

You need to be prepared to face this potential loss before you drop several hundred thousand dollars.

2. A mortgage isn’t real tax savings

People think that they can deduct their mortgage interest from their taxes and save a bunch of money.

Be very careful here. Tax savings are great, but people forget that they’re saving money that they ordinarily would never have spent.

That’s because the amount you pay out owning a house is much higher than you would for any rental when you include maintenance, renovations, and higher insurance costs, to name a few of those pesky phantom costs.

So although you certainly will save money on your mortgage interest specifically, the net-net is usually a loss. As Patrick Killelea from the real-estate site patrick.net says, “You don’t get rich spending a dollar to save 30 cents!”

What to invest in instead

As you can see, although there are exceptions, in general, buying real estate is not a great investment for individuals.

Instead, I recommend conservatively investing in the stock market. Just look at this chart.

Yet rather than spending a few hours reading up on investing to get our finances in order, we think real estate is smarter. “Investing” in a house is so programmed into people’s minds that it’s “natural” to do.

You need to realize that buying a house is the biggest purchase you’ll ever make. When you do it, you need to understand exactly why. That means an extensive amount of research.

When I bought a car, for example, I spent months learning about every trick under the sun. I had 17 dealers negotiating with each other to get my business. And that was to save a few thousand dollars!

Buying a house the biggest purchase of your life. Why wouldn’t you spend time understanding the pros and cons of it?

I’m not saying you need to devote every spare second of your life for a year doing endless research on settlement statements and what PMI is.

But you need to know the basics, and you need to know much more for real estate—which you can’t just sell the next day if you decide you don’t like it—than you do for the stock market. You can figure out how to create a balanced portfolio by spending a few hours reading a few key books.

YOU decide if buying a house is right for you

Owning your own home is a BS sacred cow: Our parents tell us to buy a house. Our friends are impressed if we own a house in our twenties. The government literally encourages us to own a house by offering tax deductions. Homeownership is the American Dream!

The truth is, if you’re making the largest purchase of your life, you need more than a slogan—you need to take the responsibility to do some research.

You not only need to understand the basic concepts of real estate, you need to be at least intermediate, if not expert, for this expenditure that costs hundreds of thousands of dollars.

So while others (especially parents) might urge you to buy a house—“rates are so low right now!”—I hold you to a higher standard. I insist you do more than take catchphrases (“I hate paying my landlord’s rent every month”) and truly understand how real estate works.

Three years from now, I don’t want you to be saddled with a purchase that you feel cheated about…because you never took the time to learn how it works.

I’m not saying real estate is a bad purchase for everyone. But the vast majority of buyers do not understand how the math works…on the biggest purchase of their lives.

Real estate might be right for you. It might not. But do not make the largest decision of your life because it’s something you “should” do.

Ramit Sethi is a New York Times bestselling author and the founder of I Will Teach You To Be Rich and GrowthLab. He writes for over 1 million millennials every month. His personal finance and business advice has been featured in The Wall Street Journal, CNBC, FORTUNE, NPR, CNN and ABC.