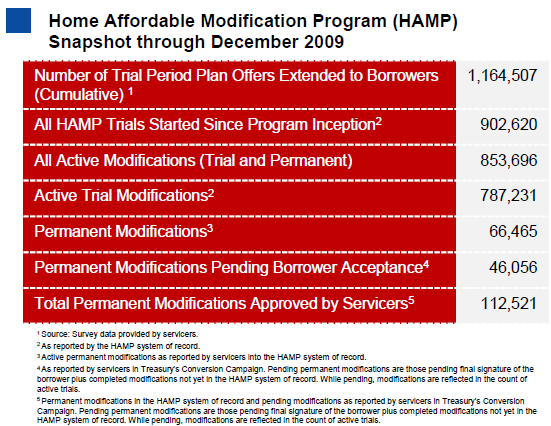

The Treasury Department reported Friday that 66,500 of the 902,620 homeowners who had started the trial modification period for its Home Affordable Mortgage Program (HAMP) had completed the three month trial and entered into a permanent modification by the end of December. Another 46,000 have satisfactorily completed the trial and have been given final documents but have not yet signed and returned them.

Although only a 7.4% conversion rate, this is more than double the 32,400 signed permanent modifications reported at the end of November.

The below chart from the REPORT provides a snapshot of HAMP progress since inception.

The primary goal of the HAMP program is to reduce the monthly payment of the borrower to no more than 31 percent of monthly income. This has been accomplished for all participants in both the trial and permanent program with a median reduction in monthly payment of $516. The median front-end debt-to-income ratio at the start of the program was 45 percent and the back-end ratio was 72.2 percent. The median of the latter ratio has been reduced through modifications to 55.1 percent.

The Treasury Department's Servicer Performance Report showed that trial plans had been offered to 1,164,507 borrowers since the program began in mid spring compared to 1,032,800 reported in November. About 101,000 homeowners entered the program in December, bringing the cumulative total to 902,620. More than 787,000 are still in some phase of the trial.

In addition to the interest rate reduction, 43.2 percent of participants have received an extension in the term of their loan and 26.6 percent were granted some form of principal forbearance in order to reach the 31 percent ratio.

The 100 percent increase in the number of loans moving to permanent status has come after much criticism of the program for its poor conversion rate. The servicers who are responsible for implementing the HAMP program have complained that borrowers are not completing the required documentation while borrowers and consumer groups have blamed the servicers for managing the program poorly, failing to respond to borrowers questions and losing the documents. The Treasury Department announced last month that it was attempted to streamline the process for borrowers and was stepping up its supervision of servicers and would even be withholding incentive payments until conversions are complete. Officials reported today that they have placed staff members on site to assist servicers and had implemented a temporary review that will extend to Jan 31 to assure that borrowers are being fairly evaluated for the program.

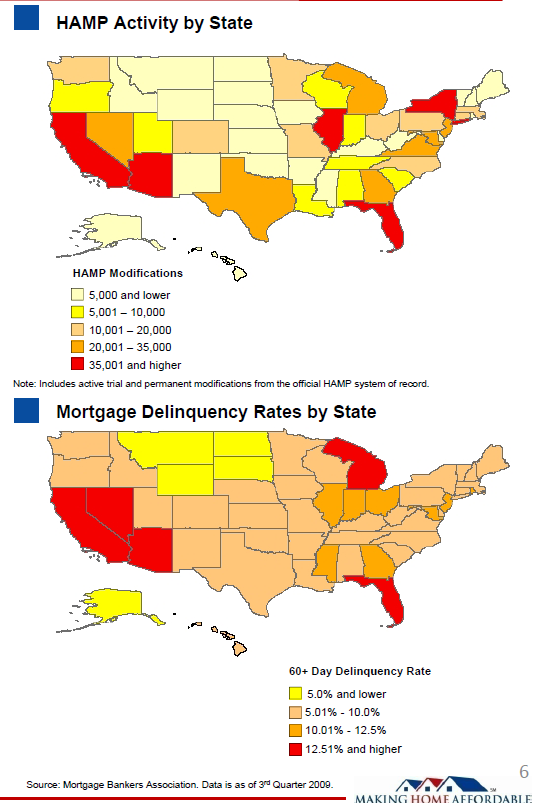

In spite of the doubling of conversions last month, the actual numbers of conversions remain small compared to the numbers who have entered the program not to mention the numbers who may be eligible to do so. In California, a state with among the highest delinquency rate, 13,353 permanent modifications have been signed out of 172,288 borrowers who have entered the program. In Florida the number is 8,405 out of 105,108, in Arizona, 4137 of 43,126. We could find no state in which the conversion rate was over 10 percent.

Here is a summary of HAMP Activity by State:

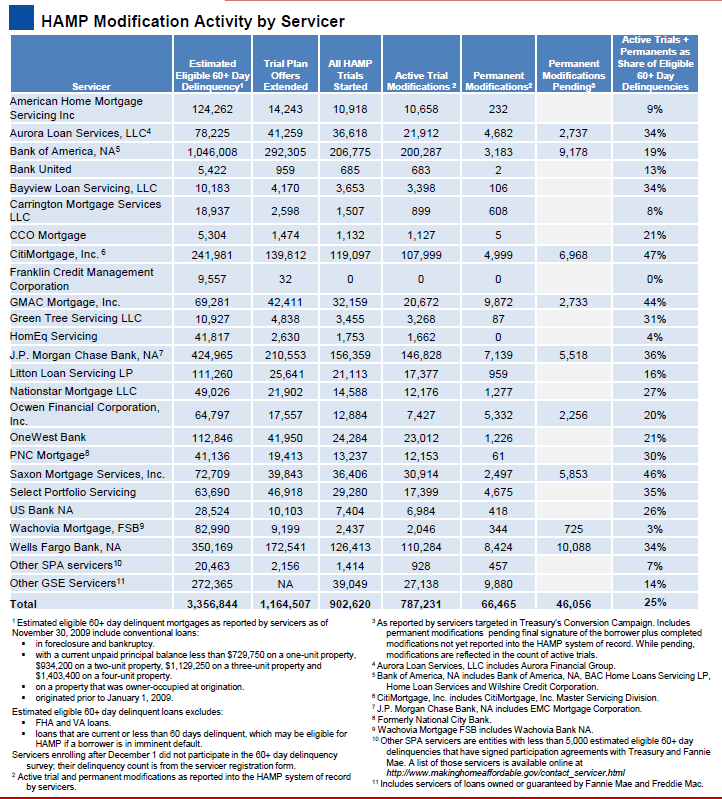

Servicer performance appears to be quite erratic, both in enrolling borrowers in the program and in converting modifications to permanent status. Citi Mortgage has the best record with 47 percent of the 60+ day delinquencies in its portfolio enrolled. However, out of 119,097 trials started, only 5,000 are now permanent and 7,000 permanent modifications are pending. GMAC and Saxon have both enrolled over 40 percent of their delinquent borrowers in the program and are both over 20 percent in completed or pending conversions. More than half of the servicers covered by the report, however, have enrolled less than 20 percent of their borrowers in trials and one servicer has enrolled none of its 10,000 delinquent borrowers in the program.

Here is an overview of servicer participation from the release:

Participants in HAMP have most commonly reported that they fell behind on their mortgage payments because of a curtailment of income. 52 percent of borrowers cited this as their hardship reason. Excessive debts were the reason given by 11.2 percent and unemployment to 5.6 percent. Illness of the borrower accounted for 2.7 percent of the reasons reported in hardship statements.

HAMP was designed to help three to four million homeowners avoid foreclosure. It requires that the monthly payment of enrollees be reduced to no more than 31 percent of monthly income and that borrowers keep payments on the modified loans current for a three month period before the changes are made permanent.

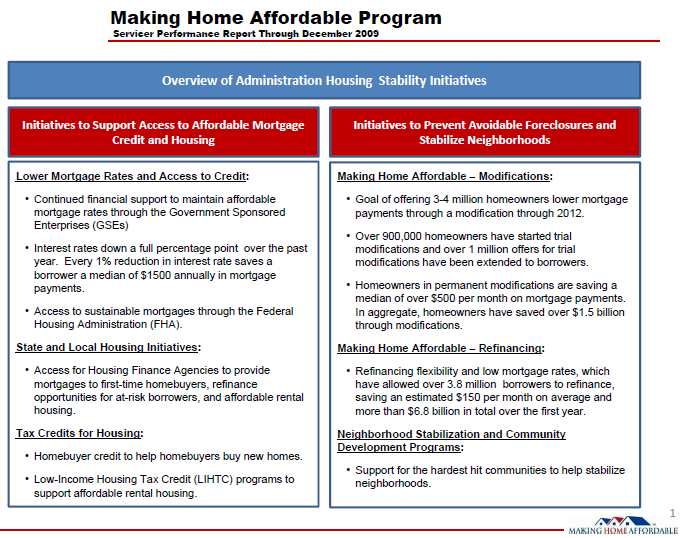

Here is an overview of the Adminstration's Housing Stability Initiatives: